As of this writing, the most recent version of the COP26 draft agreement was published early today, so it is important to understand that things are still in a state of flux.

The most up-to-date version contains an unprecedented amount of language regarding fossil fuels despite major coal, oil and gas producers petitioning to remove those references entirely. Therefore, it is possible that fossil fuels may not make it in the final text. Saudi Arabia, China, Russia and Australia have pushed significantly on this issue, and for their own good reason. If things hold and the language makes it to the final revision, this will mark the first time a Conference of the Parties climate agreement references coal, oil and gas as the biggest contributors to the human-made climate crisis.

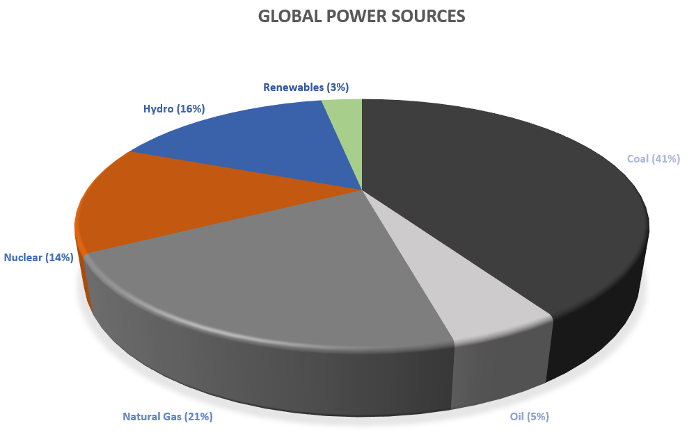

Fossil Fuels still dominate Global Electric Power Generation.

It is important to note that approximately 67% of all global electricity comes from Coal, Oil, and Natural Gas. Therefore, it is important to note that when the COP26 agreement is finalized, there must still be an accounting of what constitutes a “Zero Emissions Vehicle” dependent upon where vehicles obtain their power. But first, looking at the transportation sector, the automotive industry’s contribution to global greenhouse gases (GHGs) are from two main forms. First, the contribution of road transport – passengers and freight – related to economic activity. The UN IPCC estimates that the transport sector accounts for approximately 23% of total energy-related CO2 emissions. The IPCC also states that transport emissions could increase at a faster rate than emissions from other end-use sectors as per capita transport demand accelerates. Breaking down the transportation industry numbers, cars, trucks, buses and two- and three-wheelers – account for nearly three-quarters of just transport CO2 emissions alone.

The politics of the COP26 agreement may need to be seriously reconsidered.

Many governments allow carmakers to pool their tailpipe emissions with “cleaner” companies; meaning that if a company sells “zero-emission” vehicles, that company then becomes attractive as a partner. As an example, Tesla has perfected the art of “selling” credits to companies close to incurring heavy fines.

An important historical detail in Europe is that of diesel. In the early 90s, many countries such as the EU relied on diesel use as a way to lower CO2 contributions. And because diesel vehicles obtained 25-35% better mileage than similarly situated gasoline cars, it meant a significant total reduction in Vehicle Kilos/Miles Travelled (VK/MT). And – as governments are known to do – the move was seen as a “Magic Bullet” it meant that the EU had a “green solution” for road transport.

Things quickly progressed and EU Governments aggressively created tax regimes that favored diesel cars over gasoline and the automotive industry responded by developing diesel engine cars that were increasingly refined. No surprise – Diesels proliferated. And then – Dieselgate happened.

Once again, the globe is at a crossroads, and world governments MUST get it right.

COP26 is poised to set the course on emissions reductions from vehicles, but all the facts must be considered before policy is levied or future mistakes like Dieselgate will only compound the problem.

At present, carmakers now must invest heavily in new technologies that can make vehicles more fuel efficient (with lower CO2averages) while also rolling out more EVs to meet the new standards. Investment sums in EVs are much higher than for incumbent ICE automotive tech. Unit prices will fall as volumes rise, but that volume effect will take time. Incremental improvements to electric drivetrain cost and performance on major system components will also act to bring cost – and retail price – for EVs down. And as these new EVs roll out, competitive pressures also increase. No manufacturer can afford to miss out of market trends, and OEMs are certainly aware of such market risks. Therefore, some OEMs will conclude that it is better to sell EVs for low margin – or even at a loss – to start, if that ensures acceptable market presence and helps to avoid EU fleet average CO2 fines.

The question is: Do we have it right?

Are EVs, as “zero emission vehicles” the antidote to emissions caused by passenger cars and on-road/nonroad/off-road vehicles? COP26 must consider all aspects of EVs, and not just cherry-pick.

As discussed earlier: how is the electric power generated to charge the batteries?

It’s a sustainable source (e.g., hydro, wind) that is a good start. But if the source is a coal-fired power station, or a gas-powered boiler, that isn’t such a good thing, and is not being honest. Arguably, the CO2 is moved from the vehicle tailpipe to the power station (an “Elsewhere Emissions Vehicle” EEV) Further, Nuclear is also a much-debated energy source – though it is undeniably a good source from a CO2 point of view. In the case of France, high nuclear share in its power generation helps bring down the CO2 grid penalty for electric vehicles. It is clearly something that will vary from place to place. In the case of wind power, from day to day.

It must be noted that there is a reason why Norway (ironically rich in oil and gas reserves) was able to quickly switch to EVs. Norway has a relatively small population, much of it in and around its capital, Oslo. More importantly – it has large natural hydroelectric resources; switching to EVs was much easier for Norway than other, larger economies. A bigger country heavily vested in major ICE-based automotive manufacturing and without natural HEP resources would be at a loss.

Is COP26 working with the correct data, or is it possible that decision makers, politicians, and political action committees might be making emotional or economic decisions?

Another potential challenge that is apparently not being considered and addressed by the COP26 countries is the CO2-intensive mining requirements associated with battery materials (lithium-ion, precious minerals, etc.) Global sales figures indicate that EVs now account for 3.2% of all new light vehicle production in 2020, up from 2.4% in 2019 and a noticeable leap from 0.5% in 2015. By 2025, it is forecast that global electric vehicle production will rise four-fold to more than 10.6 million units, accounting for 10.7% by volume.

By 2030, global electric vehicle production is predicted to reach 23.6 million units, accounting for 22.1% of the total light vehicle market. By 2035, EV production is projected to be at 34.1 million units, accounting for 31.1% of total light vehicle production. Commercial vehicles are overwhelmingly diesel driven, but electric powertrains are making steady headway in light duty applications. It is partly regulatory driven, but also signals market priorities and the benefits (range) of improved battery performance. As online retail grabs more share of the retail market, delivery demand from/to distribution points are seeing strong growth.

CONCLUSION

It’s understandable to see how world governments identified as Conferences of the Parties can make a simple leap of logic:

Internal Combustion Engines (ICE) = tailpipe emissions; Electric Vehicles (EV) = no tailpipe emissions; Conclusion – ICE = BAD; EV = GOOD

Understandable, but still incorrect.

EVs may not produce tailpipe emissions (which is probably good for air quality of major city centers!) but as the data shows, EVs are not “Zero Emissions” and 67% of their global power source is still derived from Fossil Fuels. As previous Governmental decisions have demonstrated – more facts must be considered before a technology is blindly embraced and global problems are exacerbated.

Let’s hope that the COP26 Governments consider all the facts and get it right!

To learn more about the key takeaways fro this year’s COP26, please visit the UN Climate Change’s Conference Outcomes Page.